USDA loan refinance: Upgrade Your Mortgage to Fit Your Updated Budget.

USDA loan refinance: Upgrade Your Mortgage to Fit Your Updated Budget.

Blog Article

Maximize Your Financial Flexibility: Advantages of Funding Refinance Explained

Funding refinancing offers a critical opportunity for individuals seeking to improve their economic freedom. By protecting a lower rate of interest rate or changing lending terms, consumers can efficiently lower regular monthly repayments and boost money flow.

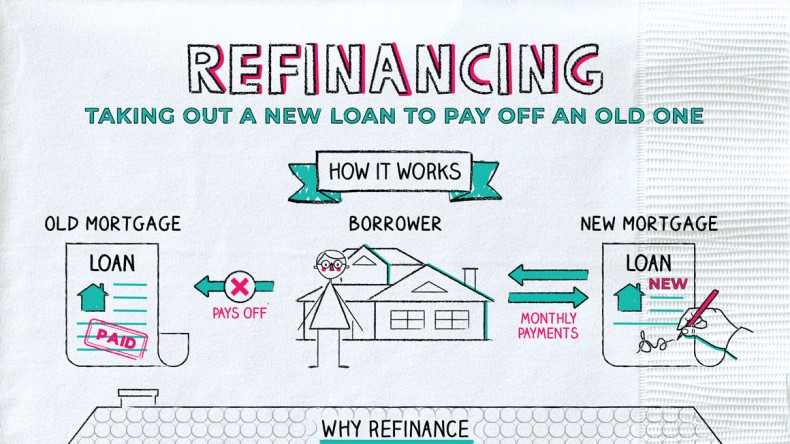

Understanding Funding Refinancing

Recognizing finance refinancing is necessary for house owners seeking to maximize their financial circumstance. Financing refinancing includes replacing a current home mortgage with a new one, commonly to attain better loan terms or problems. This monetary approach can be employed for different reasons, consisting of changing the funding's duration, modifying the type of rate of interest, or combining financial obligation.

The main goal of refinancing is usually to lower regular monthly repayments, thereby improving money flow. Homeowners might also re-finance to accessibility home equity, which can be utilized for considerable expenditures such as home improvements or education and learning. Additionally, refinancing can use the opportunity to switch from an adjustable-rate home mortgage (ARM) to a fixed-rate mortgage, providing more stability in regular monthly payments.

Nevertheless, it is crucial for house owners to evaluate their economic conditions and the linked costs of refinancing, such as closing expenses and charges. An extensive evaluation can help establish whether refinancing is a prudent choice, stabilizing potential financial savings against the preliminary expenses entailed. Inevitably, recognizing lending refinancing empowers property owners to make educated choices, improving their monetary well-being and paving the way for lasting security.

Reducing Your Interest Rates

Numerous home owners seek to reduce their rates of interest as a key inspiration for refinancing their home loans. Lowering the rate of interest can substantially reduce regular monthly repayments and overall loaning prices, allowing individuals to allot funds in the direction of other economic objectives. When rate of interest decline, refinancing offers a possibility to protect an extra desirable financing term, eventually enhancing monetary stability.

Refinancing can result in considerable savings over the life of the loan (USDA loan refinance). Lowering a rate of interest price from 4% to 3% on a $300,000 home mortgage can result in thousands of dollars conserved in rate of interest repayments over 30 years. Additionally, reduced rates may enable house owners to repay their lendings quicker, thus enhancing equity and decreasing financial debt quicker

It is vital for property owners to analyze their current home loan terms and market problems before determining to refinance. Assessing possible financial savings versus refinancing costs, such as shutting fees, is critical for making an informed choice. By benefiting from reduced rate of interest, property owners can not only improve their monetary liberty but likewise produce a more safe financial future for themselves and their family members.

Combining Financial Obligation Properly

House owners commonly find themselves managing numerous financial obligations, such as bank card, individual lendings, and various other financial commitments, which can lead to increased stress and anxiety and complex monthly payments (USDA loan refinance). Combining debt effectively with financing refinancing uses a streamlined option to handle these monetary concerns

By refinancing existing finances right into a solitary, extra convenient lending, house owners can simplify their settlement process. This technique not only lowers the variety of wikipedia reference month-to-month repayments but can also lower the total rates of interest, depending on market conditions and specific credit score profiles. By settling debt, house owners can allot their sources much more efficiently, liberating money flow for essential costs or financial savings.

Adjusting Car Loan Terms

Readjusting funding terms can substantially affect a home owner's financial landscape, particularly after combining present financial obligations. When refinancing a Continue mortgage, consumers can change the size of the loan, rates of interest, and payment routines, aligning them much more carefully with their current financial circumstance and goals.

As an example, prolonging the lending term can reduce monthly repayments, making it simpler to take care of cash money circulation. Nonetheless, this might cause paying more passion over the life of the financing. Conversely, going with a shorter financing term can lead to greater month-to-month repayments however significantly decrease the total passion paid, permitting customers to develop equity more promptly.

Additionally, readjusting the rate of interest can influence overall cost. Homeowners might change from an adjustable-rate home loan (ARM) to a fixed-rate home loan for security, securing in lower rates, especially in a positive market. Additionally, re-financing to an ARM can give lower initial payments, which can be beneficial for those anticipating a boost in revenue or financial scenarios.

Improving Capital

Refinancing a mortgage can be a critical technique to boosting cash money flow, allowing borrowers to assign their funds better. By securing a lower rates of interest or expanding the finance term, house owners can substantially decrease their month-to-month home mortgage repayments. This immediate reduction in costs can free up funds for other vital demands, such as repaying high-interest debt, saving for emergencies, or buying possibilities that can yield greater returns.

Moreover, refinancing can give debtors with the choice to convert from an adjustable-rate home mortgage (ARM) to a fixed-rate home mortgage. This change can stabilize monthly repayments, making budgeting less complicated and enhancing monetary predictability.

An additional avenue for boosting cash circulation is with cash-out refinancing, where home owners can obtain against their equity to gain access to liquid funds. These funds can be made use of for home renovations, which might raise property value and, subsequently, money flow when the home is offered.

Verdict

Finally, loan refinancing presents a strategic possibility to enhance financial liberty. By reducing rate of interest, consolidating debt, changing loan terms, and enhancing cash money flow, people can attain a much more positive economic position. This method not only simplifies settlement procedures yet additionally promotes reliable resource allowance, ultimately promoting lasting economic safety and versatility. Accepting the benefits of refinancing can result in considerable enhancements in overall economic health and wellness and stability.

Report this page